In the aftermath of various lockdowns that led to divestments, delays in expansion plans and in some cases, bankruptcy, the crisis also offered new opportunities to existing and new players to improve their market penetration across the African retailing landscape.

Christele Chokossa, consultant at Euromonitor International

Such dynamics transformed the competitive landscape between local and international players, a trend consolidated by the momentum gained by franchise models. As a result, the race to leadership in Africa depends on retailers’ abilities to adapt to a complex operating environment and meet needs from evolving consumers' behaviours.

The ‘Made in Africa’ labelling will become more relevant

Before the pandemic, African governments relied on policies like tax incentives and import restrictions to encourage retailers to source their products locally. However, the concept of ‘Made in Africa’ has gained more traction over the past few months to become a crucial part of retailers’ long-term strategy, thanks to disruptions in the global supply chain and rising logistic costs as the world re-opens.

Interest in ‘Made in Africa’ is also reiterated by a persisting inflationary pressure and currency depreciation which negatively affects purchasing powers across import-dependent countries like Angola. In parallel, the momentum gained in the sustainability trend leads to more stakeholders calling for a supply chain that integrates local small and medium businesses.

In line with this trend, major retailers will likely prioritise the development of an efficient route to markets, leading to more 'glocalised offerings'. The shift will be consolidated by a faster implementation of the African Continental Free-Trade Agreement (AfCFTA), which has been ratified by up to 38 states members in late 2021.

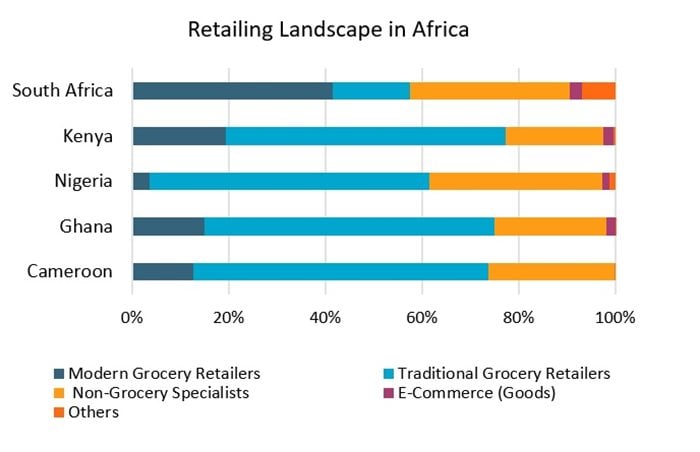

Modern grocery outlets going smaller but closer

As the emergence of new variants continues to affect footprints across crowded areas such as shopping malls in countries like South Africa, leading retailers are likely to bet on smaller convenience stores formats to meet changing shopping behaviours.

In the least developed markets like Ghana and Uganda, chain stores will leverage their economy of scale and the expansion of smaller shopping centres in peripheric urban areas to improve their market penetration across high and middle-income neighbourhoods. Beyond proximity to households, this approach will allow such companies to manage their liquidity more efficiently during the recovery and, might also become a viable entry strategy over the long term.

However, the shift will meet an evolving traditional and informal retailing landscape, with the sector receiving more support from fintech, such as Twiga in Kenya and Alerzo in Nigeria. Increasingly backed by global investors through seed funding and strategic partnership with leading financial service providers such as Mastercard, the expansion of fintech solutions focusing on providing more operating efficiency to the informal and traditional is set to intensify competition with modern retailers.

Source: Euromonitor

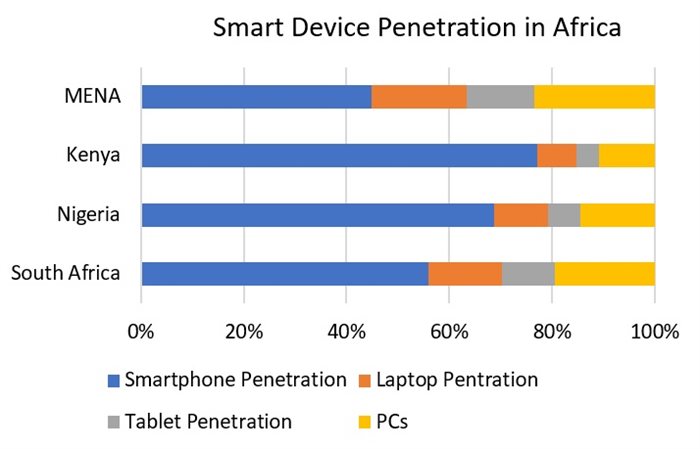

The leapfrog into m-commerce services

The influx of entry-level smartphones and lowering data bundle prices has been creating room for a mobile app culture in sub-Saharan Africa, and subsequently, m-commerce services. The trend also benefits from the diversification of leading telecommunication companies such as MTN Group and Vodacom in the financial landscape, with mobile money making its way from physical stores to online platforms during the reviewed period, backed by over 500 million users across the continent.

The adoption of m-commerce services will be accelerated by the modernisation of payment systems across the continent as it facilitates transactions with the overwhelming number of unbanked populations, and therefore overcome payment and safety challenges experienced so far. A noticeable example can already be taken from the launch of the e-naira in Nigeria in 2021, and the imminent implementation Rapid Payment Programme (RPP) in South Africa which both offer an efficient digital solution across income groups.

In parallel, the emergence of new business models such as ‘last mile to intermediary’, which conveniently leverage an existing network of traditional outlets and third-party pick-up points to bridge the digital gap will mitigate persisting geo-mapping concerns faced by operators.

As the trend unfolds, online marketplaces will face intensified competition from social commerce services, with many consumers embracing the affordability and conveniences of services like WhatsApp for businesses which has been adding value to small and medium businesses services such as direct selling so far.

Source: Euromonitor

In conclusion, combined effects of steady economic growth, low market penetration in modern retailing, and a rising population will continue making Africa a viable destination for retailing businesses. Nevertheless, the support of fintech is also likely to take traditional and informal retailers to the next level, and therefore, setting the pace for a more competitive landscape.

As a result, successfully tapping into the African market will require operators to adapt to the evolving operating environment, and this implies developing models that improve flexibility, efficiency and affordability.