In this paper, Ipsos examines the reasons for such variance in outcomes. Brand Desire and Market Factors both play an important role in contributing to the success or failure of brands, and a thorough understanding of the African consumer is vital for understanding how these elements apply uniquely to this market.

People buy brands. So an understanding of and insight into these people is necessary if brands are to pursue business opportunities in Africa. They must explore their background, outlook on life, priorities and behaviour before they can understand, measure and grow brands and establish brand equity.

People living in Africa largely find themselves in different circumstances from an economic, social and environmental point of view to the developed or ‘Western’ world. The African middle class have different priorities. There are some deep-rooted tension points that concern them.

There are also unique influencers when it comes to purchase decisions in Africa. Key drivers of brand choice in Sub Saharan Africa are quality (36%); affordability (18%), availability (13%), convenience (10%), and popularity of brand (8%). Even when money is tight, best price or value for money are, interestingly usually not the key drivers of choice

Quality is an overarching influence when it comes to food purchases. Health concerns are of utmost priority. There is a preference to buy and consume traditional foods versus packaged food from a store, because they are believed to be healthier and provide more nutritional value than their pre-packaged alternatives.

Purchase decisions are made with a shortlist of alternative brand options in mind: this shortlist comprises a set of brands that a person feels comfortable enough to purchase at the moment of choice. This shortlist is limited to 4.7 brands in developed markets (compared to four in emerging markets), whereas in Sub Saharan Africa it is only 3.7 on average, and in South Africa, this set of brands is only made up of 3.4 alternatives1.

This seemingly simple concept of understanding the number of brands on the mental shortlist is oftentimes an explanation for the failure of brand growth. If a brand isn’t on the shortlist, its chances of being bought, are indeed slim. Marketers therefore need to identify which brands are already on the shortlist, in addition to understanding how to get onto it for any given category.

It’s likely that the number of brands in the mental shortlist is influenced both by people’s appetite for variety and demands for increased choice, as well as what is physically available. In developing markets, the variety of offerings is often more limited and is not expanding at such a similar rate - and hence the available choices are already curtailed.

The variability of disposable income in the African middle class may also play a role, where there is likely to be a greater tendency to stick with the few brands people have experienced, know and trust in order to avoid a potentially expensive mistake by buying something unknown or new.

Interestingly yet perhaps not surprisingly, the number of brands in the mental shortlist has shown a gradual increase in the developed world with an average of one additional brand being included on the list now compared to seven years ago. In Africa, the number of brands on the mental shortlist has in fact remained flat over time2.

Brands that aren’t on this very limited mental shortlist are typically screened out and advertising has little impact on those for whom the brand isn’t relevant. But understanding how to drive up consideration of brands from the periphery and onto the shortlist is paramount to brand growth.

Commitment theory states that relationships are a function of two overarching dimensions: functional performance (how well it delivers on what it promises to do) and the emotional connection it can create. For brands to build relationships with people, they need to fulfil two key roles: emotional connection and functional delivery3.

Building emotional connections is important but can be more challenging than convincing audiences of superior functional performance, which is more easily communicated and demonstrated.

Average emotional connection ratings are generally lower than functional performance ratings - and this is a universal observation, noted across developed and developing regions, as well as in Africa. This, together with the observation that people tend to rate brands on the lower end of the scale for the emotional connection compared to functional performance in Sub Saharan Africa might indicate that building emotional connections is actually harder to achieve in SSA.

But what we know from independent research4 is that when two brands are equally loved, it is an improvement in the emotional connection a person has with the brand that can swing that brand to becoming the best or most favoured brand on the mental shortlist.

Market forces, such as stock availability, limited ranges, expensive prices and limited or non-existent promotional activities can change shopper behaviour and prevent people from buying the brands they want, and push them towards alternative brands.

These factors play a more substantial role in altering purchase behaviour in Sub Saharan Africa for market leading brands than they do in developed markets. The presence of these market factors contributes 4.25 additional market share points to the market leader’s overall brand equity score - meaning the brand gets more market share that it should because people can’t buy the other brands they want to due to one or other limiting reason.

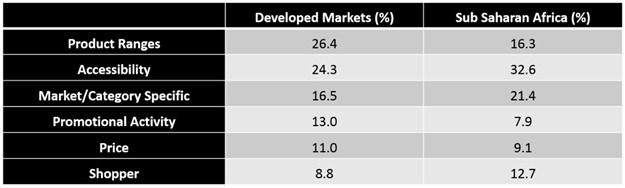

It is often assumed that price is the biggest barrier that gets in the way of people buying the brands they want. In Sub-Saharan Africa and South Africa however, the single biggest barrier impacting on purchase behaviour is related to accessibility - a barrier that is in fact increasing in prominence as the leading market factor over the last few years.

Price-related factors (i.e. being too expensive) only accounts for between 9% and 11% of overall barrier contributions across regions; it is the fourth biggest influencer, whereas in Sub Saharan Africa it is surprisingly only the fifth most impactful element (see Table 1).

Why should an understanding of how accessible your brand is, be of great interest to brand owners? In Africa, the channel of choice for buying perishable items is open air markets, whilst items like dairy, beverages and packaged goods tend to be bought in small neighborhood stores or supermarkets; usually paid for in cash. If the biggest barrier to purchase in such shopping environments is due to accessibility, this indicates potential for brand owners to reconsider their distribution activities and stock management in relevant channels.

Product range factors (for example, the product does not come in the desired variety / flavour / packaging / format) constitute about 16% of the elements that prevent purchase behaviour, yet this factor too, has almost doubled its contribution to all Market Effects over time. The African Middle Class is also more open to experimenting now than ever before, which may be due to their increased exposure to variety given their increasing online presence. Despite the limited number of brands they consider, this group of people is seeking more variety - but that sought-after variety is lacking, and they are hungry for it.

Let us pause for a moment to reflect on these product range frustrations experienced in Africa, and how they’ve increased over time. For consumable products, we know that high quality and good nutritional values are important, as is having a real appreciation for ‘the local flavour’. Given the preference of African / local branded goods, yet appreciating the perception of better quality for international brands suggests that opportunities exist for brands that want to invest locally appreciate and deliver on local nuances through their branded offerings.

There is hard evidence to demonstrate the impact of the role of the purchaser. Shopper-related market forces is a key barrier to purchase in Sub-Saharan Africa, and is a unique phenomenon at that, accounting for 12.7% of all barrier contributions (it is less than 9.5% in other regions). Included in this type of barrier are elements related to preferences of the main shopper or those of the household: for example, a brand isn’t bought for the household by the main shopper for one or other reason, or a brand isn’t bought because it is not the preference of the household.

Whilst it is the accessibility barrier (and not price as one would immediately assume) that is by far the single biggest element that impacts on people’s ability to buy the brands they want to buy, it is also important to remember the impact of quality as noted earlier: people will choose from what is available based on a quality perception, more so than how much it costs.

One final, yet important point about the in-market forces that influence shopping behaviour is that there is a host of market and category-specific elements that are more evident in Africa than in the developed world. This accounts for 21.4% of the market forces that impact purchase behaviour in Africa, versus only 16.5% in developed markets.

The ease of product use is one such example. Cleaning agents, for instance, might require water for effective use; however, water isn’t always accessible or available ‘on tap’. Complicated loan approval processes may heavily influence the uptake of products in the financial sector; products not being available cold due to lack of refrigeration or electricity may seriously impact confectionary brands as well as beverage brands (alcoholic and non-alcoholic) and not having enough payment options in retail outlets are all very real and very specific factors outside of the conventional in-market factors we observe in the Developed world.

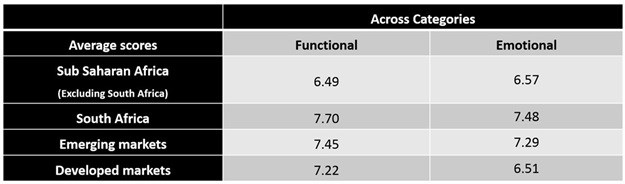

When we look at the average scores of the functional performance and emotional connection rating questions, both with point-in-time and over time differences, we can see some evidence of cultural bias.

For example, as highlighted in the table below, average Brand Performance ratings amongst brands on the mental shortlist is very different across regions overall and within the sub categories of FMCG and alcoholic beverages, with South Africa typically scoring higher and Sub Saharan Africa typically scoring lower. Interestingly, the performance expectation is higher in all regions for the FMCG category in all regions besides in developed market, where it is marginally higher in alcoholic beverages.

So where does this leave us in creating a universal measure of brand equity? Instead of using the scores of the functional and emotive dimensions as they are as inputs into equity modeling, we transform them into a rank order instead. Using this approach, if some cultures tend to rate highly and others lower, the cultural bias effect is eliminated and the playing field is leveled. There is no resultant impact on the metrics we use for the measurement of brand equity.

Brand Performance is always rated higher than Closeness (except for alcoholic beverages in Sub Saharan Africa, excluding South Africa). We can deduce that for a brand to be considered for purchase or use, it needs to meet a level of basic performance i.e. deliver on what needs there are in the category: this is a category hygiene factor. Some brands are better at this than others, but if a brand doesn’t perform, one could argue that it probably doesn’t make it onto ‘the shortlist’ in the first place.

Our data shows that smaller or challenger brands (they could be new entrants, premium brands, niche brands or just plain small brands) are characterised by lower average functional performance and emotional connection scores; whereas market leading brands always enjoy higher average scores on these important relationship measures7. This pattern of higher scores amongst brands with higher market positions is a universal observation, noted across categories and across regions around the globe.

This observation demonstrates the sheer importance of focusing on building up the brand relationship dimensions in any marketing strategy - especially given the mental shortlist constraints prevalent in Africa. The learning from the market leading brands relationship metrics is clear: the better your brand is believed to perform on what it promises to do, and the more emotionally connected your consumers are, and the more beneficial it is for your brand’s overall equity and position in the market.

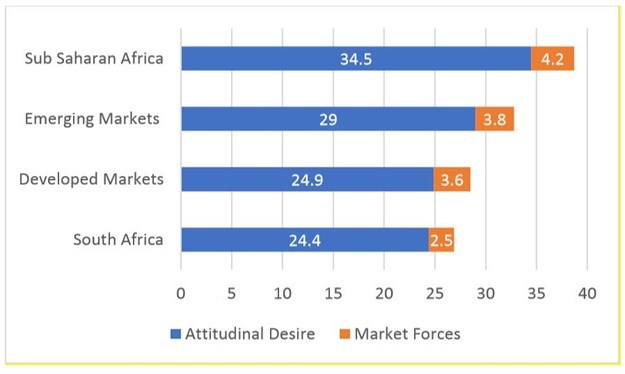

Market leaders take ‘more than their fair share’ in terms of their overall market share. Leading brands are bought more than they are desired, because other brands suffer from the impact of in-market forces that prevent people from purchasing them when they want to. And we can see the evidence of this when we look at the equity scores for brand desirability (the attitudinal component) and the factors that prevent people from purchasing brands (the behavioural component) for market leading brands - especially in Emerging Markets and SSA (without SA) where the top ranked brand gains the lions share, and the gap between leader and follower is substantial.

In Developed markets, a market leading brand is expected to have an attitudinal brand desire score of 24.9% (which, given the model’s validations with real business outcomes, will be a similar value to its actual market share), whereas in emerging markets it is higher at 29%, and in Sub Saharan Africa it is a substantially greater 34.5%. South Africa, interestingly, shares a similar expectation for the number one brand as developed markets, at only 24.4%.

The impact of market forces which change actual purchasing behaviour (which is made up of the accessibility, price, product range factors described earlier) is very interesting. In Developed regions, the average positive impact of market forces on a brand’s total share is 3.6 share points, 3.8 in emerging markets and as high as 4.2 in Sub Saharan Africa, whereas it is only 2.5 additional share points in South Africa. It seems that in Sub Saharan Africa, there is merit for being a market leader as desirability is high and the positive impact of market factors is even more beneficial to the brand’s overall standing in the market. Furthermore, the gap between market leader and second placed brand is substantial in the region: the market leader’s overall share is more than double the second player!8

The reality is that without saliency, or being in the consumer’s mind and on their mental shortlist, a brand has little chance of success. Building saliency is a key first step, and building a brand relationship comes next. How you get there is up for debate. But it is now generally accepted that this is not the only route a brand can employ. For a brand to demonstrate that it delivers on its promises (i.e. it does what it claims to do), it can communicate it or it can initiate trial and purchase by putting the brand in people’s hands by deploying one or other marketing technique, so that they can experience it for themselves. People who are recent users of brands typically have higher relationship ratings, perhaps a self-fulfilling prophecy, but the reason people will continue to use a brand is because it delivers on what it says it will, and they connect with it on a deeper level, to one degree or another. The creation of a solid emotional connection cannot be underestimated: the previous discussion on this topic highlighted that building the emotional connection is harder to do, but that brands that build distinctiveness and do it right enjoy the resulting benefits.

Entering with a trade marketing strategic focus via promotions, prominent on-shelf displays or price discounting may help to achieve limited and short-term saliency and begin to build the brand relationship, but it isn’t enough. A brand must build up sufficient desirability simultaneously - and it must continue to reinforce the reasons to believe in the brand throughout the brand lifecycle. Chart one shows the contribution to overall equity by the attitudinal desire versus the market forces, and the bigger contribution is unanimously the desirability component. It makes intuitive sense that the strategic focus should therefore be on building desire.

1 Ipsos Laboratories Equity database

2 Ipsos Laboratories Brand Equity Database

3 Commitment Led Marketing: Hofmeyr and Rice (2000)

4 Ipsos Laboratories R&D

5 Ipsos Laboratories Brand Equity Database

6 Ipsos Laboratories Brand Equity Database

7 Ipsos Laboratories Brand Equity Database

8 Ipsos Laboratories Brand Equity Database