South Africa’s consumer class youth is playing snakes and ladders

These are some key insights from the newly released BrandMapp Youth Report, based on the largest annual surveys of South African adults in the consumer class. It shows a picture of the economically active segment of the country’s youth: the aspirant consumers under the age of 35 whose dreams, concerns and ambitions, preferences and habits rarely make the headlines.

“High rates of youth unemployment, poverty, educational frustrations and inequalities naturally dominate our national conversations about young people,” says Brandon de Kock, BrandMapp’s director of storytelling, “but at BrandMapp, we focus the lens on the segment of our youth who are lucky to be well-educated, forging career paths. This is highly relevant because they are contributing significantly to building our economy and tax-paying base. Across all industries and institutions, we also need to be able to track how they are doing in life and understand their outlooks and motivations.”

Working towards a better future

Yet BrandMapp’s youth data highlights that the large group of young people who are part of the consumer class are neither passive nor hopeless. De Kock points out: “This segment makes up 40% of the 14 million adults living in households earning more than R10K per month, so that’s almost six million economically empowered young consumers who are leading us into the future.”

Nearly two-thirds of consumer class young adults are already participating in the workforce through employment or entrepreneurship. Twenty-three percent are students, and although 11% are unemployed, it’s a sign of their ambition that 0% of them are not seeking work.

But as BrandMapp’s youth specialist, Ashleigh Cumming, explains, there’s more to the story than meets the eye: "Contrary to the common narratives of dependency and passivity, youth consumption is not being driven solely by parental support or student lifestyles. The majority are already earning, spending and making financial decisions in the real economy. They are already on the board, but at a life stage defined by ambition and transition. The challenge is that they don’t yet have the financial security to easily deal with turbulent times, so while older generations are playing Monopoly with their cash, the younger ones are struggling to work out how to survive a game of snakes and ladders!”

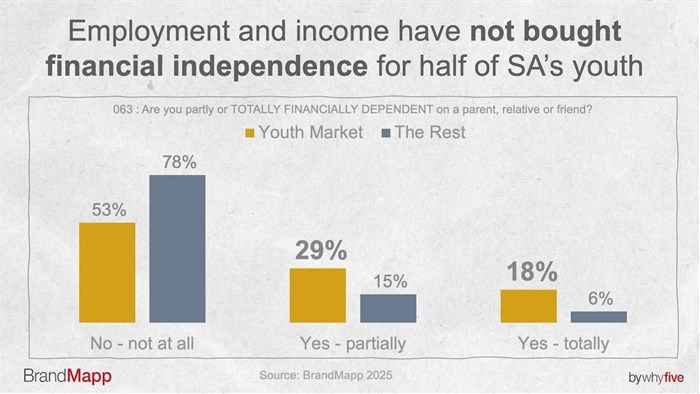

Employment alone, however, does not translate neatly into independence. More than half say they feel financially better off than they did two years ago, suggesting forward momentum, but almost half of consumer-class youth still rely partially or fully on financial support from parents, relatives or friends. The defining tension in their economic lives is participation without full arrival.

“The thing is, for younger people, progress is uneven, with everyday expenses absorbing much of the gain,” Cumming says, “and the result is a version of adulthood that feels a bit extended and fragmented rather than a straightforward path. Older generations almost certainly enjoyed a quicker journey with income naturally leading to independent living and asset building. Today, financial progress for young people is much less linear.”

Under pressure but trying to do the right thing

According to the 2025 Old Mutual Savings & Investment Monitor, savings account for 22% of household income, and working South Africans are 'more upbeat than they were a year ago' with 44% reporting higher personal income.

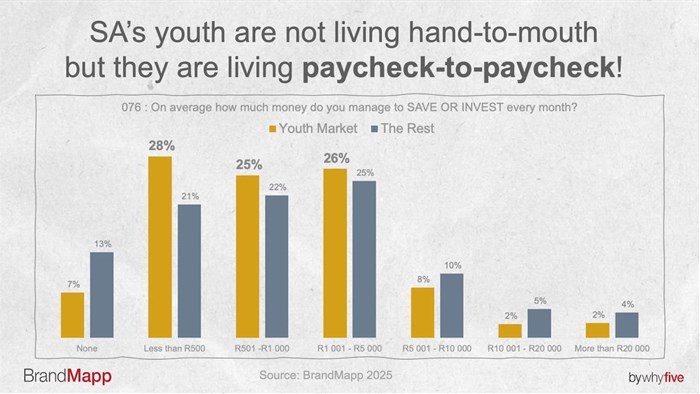

However, BrandMapp finds that a significant share of youth is saving far less than R1,000 per month. Not because saving is not prioritised, but because monthly costs consume most of their available income.

Cumming says: “The challenge isn’t simply income. It’s purchasing power. Relative salaries have not kept pace with the cost of housing, transport, education and everyday living expenses, reducing young people’s ability to convert earnings into financial freedom. They aren’t living ‘hand-to-mouth’ but they certainly are living paycheck-to-paycheck. And the good news is that they have gotten pretty good at it.”

“On paper, SA's youth are surprisingly disciplined with money. Their two dominant financial personas are the Guardian (28%) and the Saver (29%), together representing the majority of the youth market. But you can have a Guardian mindset and still be unable to save, if the economic system won't cooperate. What emerges is a generation that is financially intentional, but structurally constrained. They are stepping up ladders, but there are definitely more snakes abound on the board than what their parents and grandparents experienced!”

How are their finances affecting the way they feel about life in South Africa?

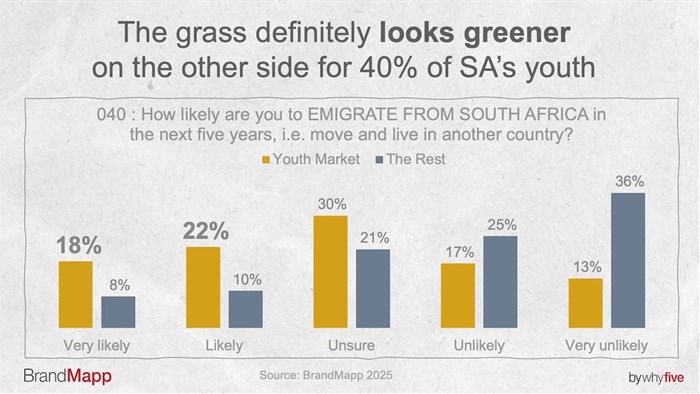

“For those of us who have been tracking the youth market for the past decade,“ says De Kock, “there are aspects of the modern world that are undeniably ‘novel’, specifically when it comes to mindset. We see a rise of mental health awareness in the age of social media, and a constant barrage of negative news that can only lead to heightened levels of dissonance and cynicism. In short, truth is a moveable feast for younger consumers. But despite all of this, young people in the consumer class are generally happier than the older generations. They are more likely to feel unsure about South Africa’s future, but crucially, they're not more pessimistic than older generations.

"The latest BrandMapp Youth Report also shows that they are nurturing serious aspirations with 46% aiming for a new job this year and 30% planning to start a business. This seems to me to be a resilience story worth telling.”

A snapshot of the forces shaping young consumer class adults’ lifestyles:

- Cultural ambition: Music, movies, socialising and travel at the top of the youth wish list, but there’s also high interest in beauty, grooming, fashion and sports that tells a deeper story of a culturally rich South African generation. This in line with the global trend of young consumers are increasingly defining identity and status through experiences, self-expression and personal growth.

- Safety-conscious, more intentional drinking: Previous generations often drank by category, driven by volume and habit. But today’s youth are drinking by occasion. A third of them don’t drink at all, and that’s widely acceptable. For those that do drink, it’s more about the experience, occasion and flavour.

- Efficiency focus: Youth are building lifestyles around efficiency and increasingly choosing solutions that help them do more with limited time and resources. Despite mistrust or scepticism in what algorithms might feed them, young people still value the speed and convenience of responsive, personalised digital advertising.

- AI fluency: While AI is still often discussed as an ‘emerging technology’, BrandMapp’s youth audience is already integrating it into everyday learning, work, creativity, and decision making.

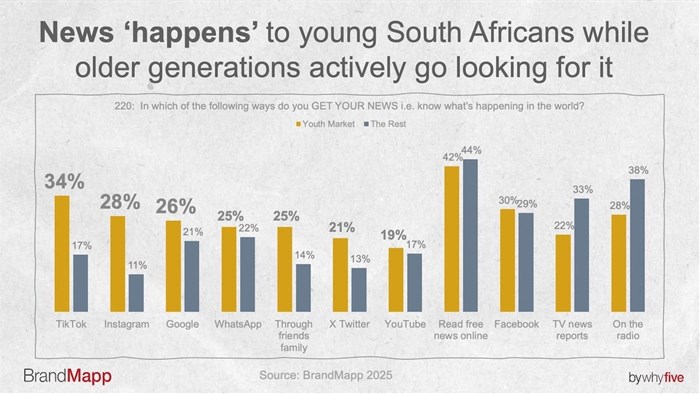

- Multi-platform media journeys: The conversations about how to reach young consumers has shifted from traditional versus digital to the ‘discover-to-purchase’ journey. For youth, social media powers how they learn, work, socialise, shop and build identity. The platforms may differ, but together they form the operating system of modern youth life. However, traditional media is not lost on them. Rather than replacing traditional media, social platforms have become the first step in a multi-platform news journey. Youth get their news through a hybrid ecosystem.

So who can they trust?

De Kock concludes: “It’s probably the most powerful insight we draw from the data: younger consumers increasingly encounter news and brands through social platforms and peer networks, but when it comes to trust, traditional media still matters. News ‘happens to them’. They encounter stories and products through friends, feeds and algorithms, but they still look to established media to determine what is credible. And at the same time, they may well be using their environmental media to determine the validity of what they see in traditional news media! In the race to capture their attention, the winners will be brands that can succeed in both environments simultaneously.”

BrandMapp 2025 insights is available directly from the BrandMapp team at WhyFive Insights and by subscription via Telmar, Softcopy, Nielsen and Eighty20. For data access email az.oc.evifyhw@enna-eiluJ.

- South Africa’s consumer class youth is playing snakes and ladders17 Jun 09:41

- The All Blacks are coming! Who cares? About 6 million consumer class adults, that’s who…26 May 10:45

- South Africa’s consumer class is back on the road!13 Apr 12:13

- South Africa’s consumer class is all in on AI19 Feb 09:56

- How are SA consumers feeling at the end of a lo-ong year?27 Nov 11:56