Africa's big 5 keys to financial transformation, inclusion

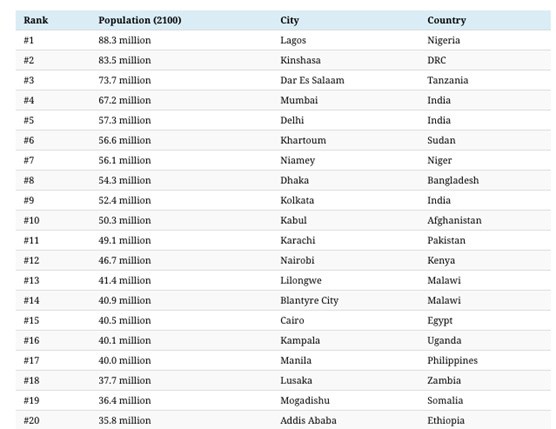

According to Visual Capitalist, 13 of the world’s largest urban centres in 2100 will be African (see fig.1 below), indicating the vast access to new markets – one which will be enhanced by dramatically different bandwidth and costs.

At a recent seminar held by TMT Finance, at the TMT Finance Africa in Cape Town 2019 event, four industry-leading panellists from PayU, Jumo, World Remit, and MFSAfrica, tackled the topic of how cross-border payments and remittances are exploding across the continent, unpacking five key transformations:

- Mobile money: The continent’s adoption of transacting has developed faster than anywhere else in the world. Where previously it would take a day to visit the bank, withdraw and deliver cash, now it happens in a few seconds. “And with mobile money, we now have access to a farmer in rural Zambia – to suddenly get working capital for their farm. Mobile money made it widespread and created peer-to-peer transfer for customers, it is definitely possible to the payment system for Africa. If you make it more solid and if you keep building it, it is definitely possible to do a payment system for Africa in the future, and not just a temporary solution. In reality, it can actually be a very serious payment mechanism, certainly in most countries,” explains Martin Vogdt, chief product officer, at Jumo.

- Global demand: High Velocity Merchants (HVMs), the fastest growing companies in the world, have woken up to the potential in Africa, as the likes of Taxify cement a foothold in Africa. Corrie Bakker, head of Business Development and Strategy for Africa at PayU, weighs in: “The difference with these players is that they are looking for credibility and capability, a single entry point onto the continent. PayU has proven itself as the industry leader across emerging markets, and we have done the ‘hard yards’ building relationships in advance in East, West and Southern Africa, enabling these high velocity clients to slipstream into the regional nodes.”

- Cross border: As businesses build out, especially with neighbouring countries, there exists the opportunity to expand into new territories. PayU’s Bakker adds, “Some clients want a multi-country payments partner, some want to focus on the whole region – East, West or South, for example – and the larger companies want to approach the continent. One of the challenges lies in the need to clear dollars in some of these countries, due to anti-money laundering regulations, so the forms are as complicated for smaller sums as they are for larger sums of money.”

- Regulation: On the one side, banks and regulators are starting to wake up and are becoming more sophisticated, tech-savvy, communicating more and adapting. But on the flip side, terrorism and anti-money laundering bring hurdles of their own, when dealing in dollars. “We did a survey not too long ago, 55% of the users of our service between Uganda and Kenya are using it for business purposes; self-declared. So, and you like it because it’s a quick way and easy way to settle trade and so on. But because both Uganda and Kenya needs to clear dollars, now we’re having to ask two hundred questions for someone to say 100 dollars,” explains Dare Okoudjou, CEO of MFSAfrica.

- Financial inclusion: The increasing number of solutions is driving down cost and delivering more options, allowing senders and receivers more choice. Originally, payments were dominated by card transactions, and were largely bank driven, but Fintech has introduced QR codes, Zapper, SnapScan, as a few examples, and, in addition, media platforms such as WhatsApp and SMS are helping customers to talk and transact more easily. Technology has also ‘increased the pot’ significantly, bringing women and teens into the equation, driving financial inclusion, especially for the mothers and grandmothers in the household.

“For example in Tanzania, 91% of our volume is going to rural areas. Historically, that was not the case because individuals would have to leave the village and come into an urban area, find an agent and get the cash. That would be almost a day’s experience, and unfortunately on the way home there’s significant leakage for whatever reason. So for mobile-to-mobile you can now send directly to the intended recipient and then that money is theirs to use for its intended purpose, be it education, staple food stuffs, or other. For this reason, individuals will send in more often, yes often it’s low of value, but they send two to three times more per month,” concludes Andrew Stewart, managing director EMEA, of World Remit.

As the world sits up and takes notice of Africa, the pieces are slowly beginning to fall into place as innovators across the industry unite suppliers, seek to overcome regulatory challenges and building an infrastructure that can sustain the volume that Africa will be delivering as bandwidth increases, data costs decrease and smartphone proliferation brings hundreds of millions more online.