More than a year after the outbreak of Covid-19, the global economy has begun to roar back to life, with Covid-19 restrictions easing in some countries, allowing life to resume to an extent. This has spurred global real estate markets, with issues such as flight to quality, ESG and war for talent coming under sharpened focus.

Tilda Mwai, senior analyst for Africa at Knight Frank

And across Africa, these themes are intensifying. While the pace of recovery may vary from country to country, below we examine three themes that will shape the African real estate market in 2022.

Widening gap between prime and tertiary assets expected

Across the continent, prime offices demand is making a comeback. Occupier requirements are up sharply, driven in part by the return to business confidence in regional hubs such as Nairobi, Lagos and Johannesburg. New space requirements increased by 49% in Q3 2021 compared to Q2 2021, driven in part by the professional services and financial services sectors. In stark contrast and in line with global trends, demand for more secondary stock remains low, resulting in increased concessions such as increased rent-free periods in cities such as Kampala from the typical one month to 2-3 months.

From aligning their corporate brand and image, reducing costs to ensuring employee wellbeing, majority of the occupiers now view real estate as a strategic device within their business, according to last year’s Your Space report. As such, flight to quality is only expected to intensify across the continent, with occupiers keen to occupy space that places employee wellbeing above all else. Inevitably, this will see the gap between prime and tertiary assets widen, leading to the emergence of a distinct two-tier market across most cities.

Green is the new black

One theme dominated headlines, markets and investment decisions in 2021: ESG – environmental, social and corporate governance. No longer just “the right thing to do”, understanding and delivering on these dynamics is now a business imperative. And across Africa, from offices, residential to industrial sectors, occupiers and buyers are increasingly focused on sustainability of the buildings they occupy. While there is currently a lack of tangible evidence, we expect to start seeing a ‘green value premium’ for assets aligned with ESG. Across the continent, this is likely to materialise through ‘brown discounts’ on older stock for occupiers. This discount will continue to accelerate towards what is likely to be a cliff-edge “brown value collapse” on the not-too-distant horizon for those assets that cannot match the standards required.

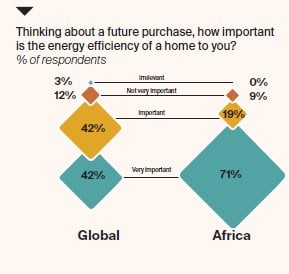

For buyers, the bottom line is what matters. More buyers are keen to occupy energy-efficient homes and even willing to pay for them. An overwhelming 71% of African respondents in the Knight Frank Global Buyer Survey indicated that energy efficiency was very important to them compared to 42% globally. In addition, more respondents across Africa (29%) indicated that they would prefer a greener home and be willing to pay more for it compared to 27% globally.

Recent climate events, a spate of zero carbon government pledges and the COP26 climate change conference, are likely to fuel this trend even further.

Source: Knight Frank

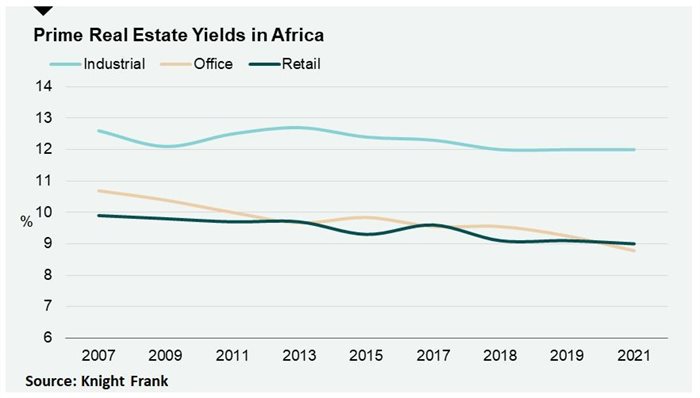

A growing investment appeal

Outside of South Africa, attracting global institutional capital across the continent has been a challenge due to the lack of investible-grade assets. However, in the global hunt for yields, investors are increasingly looking into Africa, attracted by the strong income profile and positive market fundamentals such as rising urbanisation. Indeed, real estate assets across Africa have continued to command attractive yields of approximately 12% (logistics), 9% (retail and offices) and 6% (residential).

As such, we expect increased institutional interest with players likely to invest in ‘develop to core’ situations. The proposed landmark acquisition of a controlling stake in specialist property developer Gateway Real Estate Africa, by GRIT underscores this trend.

Away from the mainstream residential and commercial markets, the push for diversification is leading to a growing preference for alternative asset classes such as data centres. Johannesburg continues to be the leading data centre market across Africa and saw 68MW of new supply being added into the market in 2020.

In addition, increased take-up activity expected in 2022 is driving new supply even further. Markets such as Nairobi and Lagos continue to undergo expansion, with new data regulations and a large increasingly connected population amplifying demand. Already, key operators such as Africa Data Centres are ramping up supply into these markets with this trend expected to continue well into 2022.