According to Compuscan's data, the average South African borrower is 42 years old, has a predicted income of R13 147 and a credit score of 618 (high risk) [see editor's note]. Furthermore indicating the situation at hand, 41% of the 22.5 million credit-active consumers in the country are considered very high risk borrowers and an additional 15% of credit-active consumers are considered high risk borrowers.

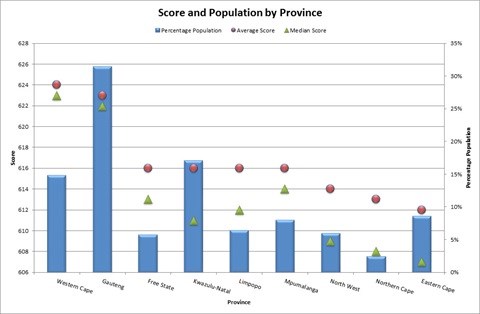

The graph indicates the percentage population, average score and median (the value right in the middle) score. The provinces are sorted by descending average score.

The Western Cape has the highest average score, followed by Gauteng; with the Eastern Cape having the lowest average score. However, Gauteng has the highest percentage of the population (read population values from the axis on the right) and the Eastern Cape's population is high as well.

The median-values are important as well. The median score for the Eastern Cape is even lower than the average, which means that the average sketches a 'rosy' picture and is being pulled up by individuals with high scores who don't constitute a large percentage of the population. The median therefore shows that individuals in the Eastern Cape are a lot less creditworthy than the average person in the Western Cape and Gauteng and even Mpumalanga, where the median is closer to the average.

Comments Frank Lenisa, Director at Compuscan: "As is revealed by these statistics, those that are considered high, and very high risk borrowers together make up more than half of all credit-active consumers in South Africa. While this is alarming, what is equally concerning is that many of these consumers may not even know what a credit score is, what their own credit score is or how a poor score is negatively impacting their ability to obtain credit."

A high score indicates that a consumer is a low risk borrower, and vice versa. It is important to maintain a good score as credit providers consider this information when deciding whether they will extend credit to you. A good credit score is paramount when purchasing a home, financing a vehicle or obtaining any other loan - your chance to obtain credit could therefore be hampered by a poor credit score.

A lack of positive credit information (which influences your credit score) can cause an application to be declined or can result in a higher interest rate, which will increase the 'cost of credit' and will have a notable impact on the amount that you need to repay.

Your credit score is calculated using the information contained on your credit report, including account information, your payment history, adverse information, public records and enquiries (requests by credit providers to view your credit report). It is a summary of both positive and negative factors that predicts how likely you are to honour your future credit agreements. Your credit score will however differ at each of the registered South African credit bureaus as they are calculated differently at every institution.

Understanding the information on a credit report could seem like an overwhelming task, and for this reason, some consumers may avoid checking their reports on a regular basis. By law, South African citizens are entitled to one free credit report every year; however, it is recommended that you carefully examine your credit report once a month, so as to monitor your financial standing as well as to identify and combat fraudulent activity.

In order to make this process easier, Compuscan has created a simple and user-friendly personal online credit portal called My Credit Check whereby South African consumers with valid identity numbers are able to monitor the complete record of their credit history, their borrowing habits, re-payment trends and contact details. Information is clearly grouped and thus you are able to easily deduce what data is having the biggest impact on your credit score and finances.

As part of My Credit Check, a new offering, "What's My Score" has just been launched. This package enables you to stay on top of your financial standing by receiving your credit score via SMS on a monthly basis for a small fee.

Your credit report is a complete record of your financial history, which contains your personal information, others' perception of your creditworthiness, your account data, dispute information and a credit action plan (to assist you in improving your credit reputation).

Important information that you should take note of on your credit report includes the following:

There are a number of simple steps that can be followed in order to build a higher score. You should:

Lenisa concludes: "It's never too late to begin working towards a higher score. As we start a new year, it's the perfect opportunity to be proactive and start making the effort to improve your credit score. After all, it could be the difference between you being able to purchase your dream house, finance a vehicle or further your studies one day, or not."

Go to www.compuscan.co.za for more information or www.mycreditcheck.co.za to access your credit report.