Insurance & Actuarial

Strong ombud performance reflects Miway’s ongoing commitment to fairness

MSL South Africa 30 Jun 2026

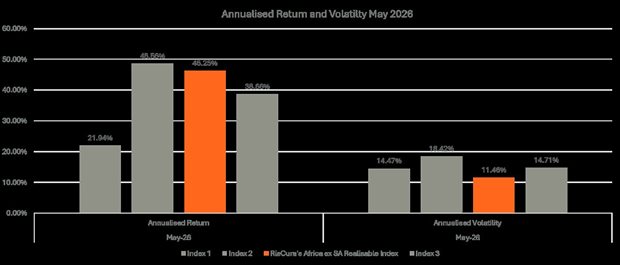

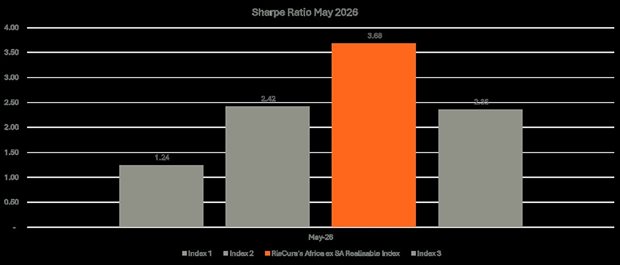

Benchmark choice can reshape African equity performance, RisCura findsThe way an investment benchmark is constructed can significantly influence how portfolio performance is measured and interpreted, according to new analysis by RisCura.  Source: Supplied. George Tsinonis; Head: Investment Analytics, RisCura. Comparing several widely used Africa ex-South Africa equity indices, the research finds that differences in benchmark methodology can materially affect reported returns, volatility and risk-adjusted performance. Over the period analysed, RisCura’s realisable methodology consistently outperformed several traditional benchmarks, with the performance gap widening over time, highlighting the importance of benchmark selection for institutional investors. What this means for institutional investors is: if the benchmark is misaligned with market realities, the judgement of performance may also be misaligned. Benchmarks are not just reporting tools. They are used to assess whether a portfolio manager has added value, taken appropriate risk, or underperformed. If a benchmark does not reflect the currency, liquidity and repatriation conditions investors actually face, a manager’s performance may be judged against a reference point that is theoretically neat, but practically misleading. The same African equity portfolio could therefore appear to be outperforming, underperforming, or carrying a different level of risk depending on which benchmark is used. In markets where official and realisable exchange rates diverge, or where capital mobility is constrained, the benchmark itself can materially shape the investment story being told. “Benchmarks are meant to provide a neutral reference point for measuring investment decisions,” says George Tsinonis, Head: Investment Analytics at RisCura. “But when benchmark construction diverges from the conditions investors actually face on the ground, the resulting performance metrics can present a distorted picture.” Much of this divergence can be traced to how global index providers treat markets experiencing currency dislocations, liquidity constraints or capital mobility challenges. In some cases, markets have been removed from indices entirely when accessibility concerns emerged, even while institutional investors continued managing capital within those markets. Market access mattersRecent developments across African markets show how these dynamics play out in practice. In Egypt (2024), the Egyptian pound depreciated by more than 60% in a single day after the Central Bank allowed the currency to float more freely against the US dollar. Investors also faced delays in accessing foreign currency for repatriation. Nigeria experienced similar distortions between official and parallel exchange rates during 2023 and 2024, with the parallel market premium exceeding 60% at certain points. Insurance & Actuarial Strong ombud performance reflects Miway’s ongoing commitment to fairnessMSL South Africa 30 Jun 2026 Traditional global indices typically rely on official exchange rates, which can differ significantly from the rates investors are able to access when repatriating capital. This can create a disconnect between theoretical benchmark performance and the returns investors are actually able to realise. The RisCura Africa RealView Index (Rari) addresses these challenges by incorporating both official and realisable exchange-rate methodologies, while also accounting for liquidity conditions and market accessibility. This approach is intended to provide a benchmark that more closely reflects the conditions institutional investors face when investing across African equity markets. Differences in benchmark construction also affect how returns and risk are reflected over time. Analysis covering May 2025 to May 2026 shows that RisCura’s Africa ex-South Africa realisable index methodology, used in Rari, delivered annualised returns of 46.25% at May 2026, while maintaining volatility of about 11.46%. This suggests stronger returns without a corresponding increase in measured risk relative to the traditional benchmarks shown.  Source: Supplied. The divergence becomes even more pronounced when risk-adjusted returns are examined. Over the last year, the realisable methodology recorded the strongest Sharpe ratio, a metric that measures an investment's risk-adjusted performance, among the benchmarks shown, at 3.68.  Source: Supplied. “When volatility and returns are measured differently across benchmarks, the same portfolio can appear to carry very different levels of risk,” says Tsinonis. “That has direct implications for how investment committees interpret manager performance.” As global investors continue allocating capital to Africa’s emerging and frontier markets, accurate performance measurement is becoming increasingly important. Differences between theoretical benchmarks and realised investment outcomes may become more pronounced in markets where liquidity, currency access and capital mobility remain uneven. For asset owners and investment committees, the findings highlight the need for a more critical approach to benchmark selection and interpretation, particularly when allocating capital across complex and evolving markets. “Performance discussions should focus on investment decisions and outcomes,” says Tsinonis. “But if the benchmark itself is not aligned with real investment conditions, the measurement framework can introduce distortions that are difficult to ignore.” Ultimately, if benchmarks fail to reflect the realities of investing, they risk measuring assumptions rather than performance. |